2025 Key Takeaways

-

The 2025 NatSec100 cohort saw meaningful movement: new entrants, strategic exits, and companies rising or falling in ranking.

This churn signals real progress. The ecosystem is functioning—companies are scaling, raising capital, hiring talent, and in some cases, turning a profit. As dual-use technologies continue to mature, particularly in hardware-intensive sectors, the defense innovation base will require new financing models. Long-term success will depend not only on Wall Street’s capital markets but also on the broader support of Main Street—America’s industrial base, mutual funds, family offices, state and local governments – to ultimately deliver at scale.

-

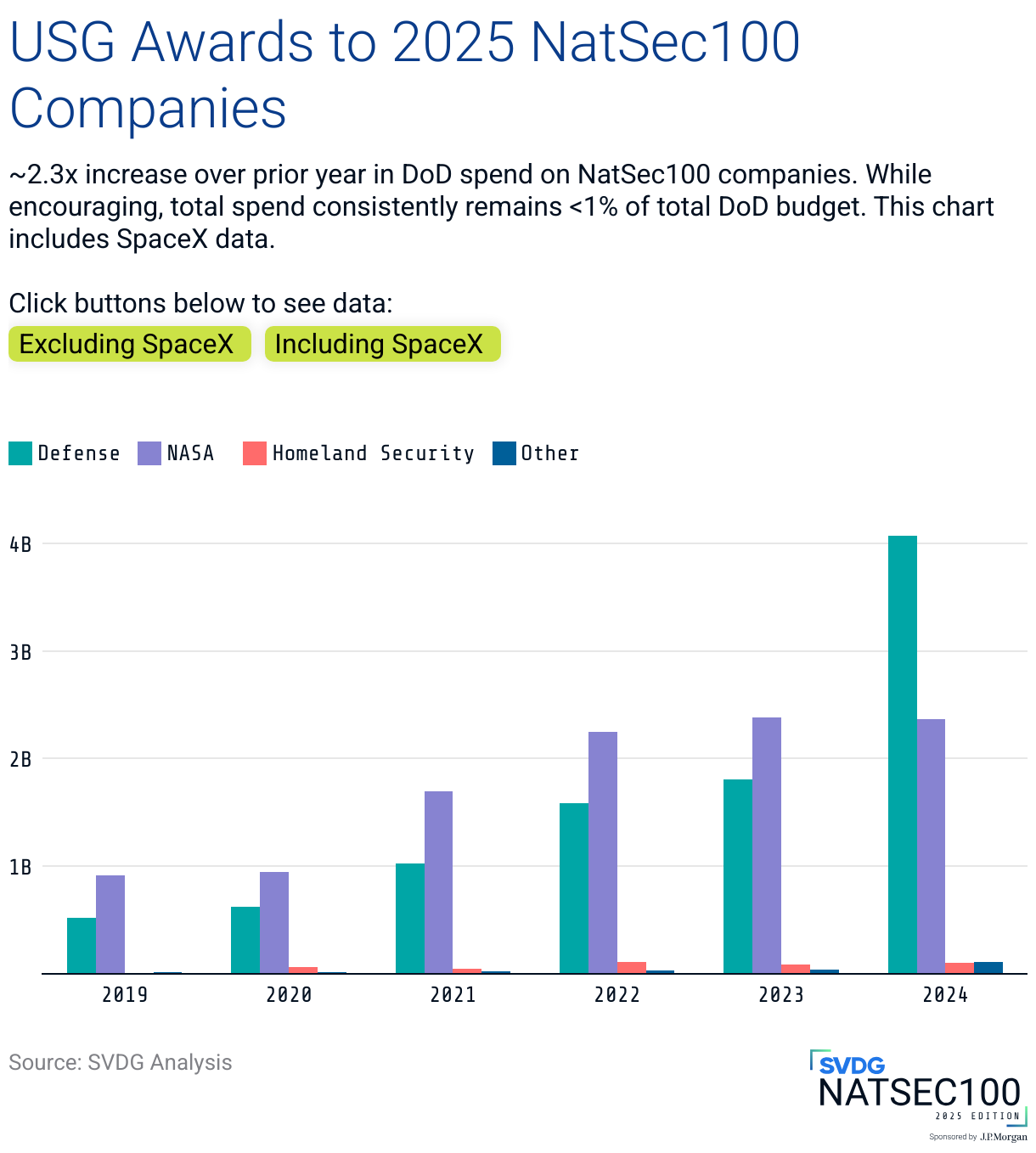

DoD spending on NatSec100 companies more than doubled from 2023 to 2024 (~2.3x), totaling nearly $4B, or $1.95B excluding SpaceX.

While SVDG was thrilled to discover a ~2.3x YoY increase in DoD spend on 2025 NatSec100 companies, a significant investment mismatch remains. The USG has awarded $28B in total historical federal awards for this year’s NatSec100 companies. Comparatively, $70.1B in total private capital has been raised for the same companies. This gap must continue to close in order to incentivize continued development and investment. Continued progress depends on DoD's willingness to take on more innovation risk and “pick winners.” Picking winners means scaling firm fixed price contracting and large programs of record for non-traditional companies.

-

In USG acquisitions, most contracts are governed by the Federal Acquisition Regulation (FAR), a robust and comprehensive set of rules and procedures for acquiring goods and services. However, contracting officers can also utilize alternative legal authorities and procedures, often involving Other Transaction Agreements (OTAs) or other mechanisms outside the standard FAR framework, referred to as non-FAR contracts. Roughly 12% of FY24 USG awards to NatSec100 companies (excluding SpaceX) were via non-FAR contracts—representing a 2x increase over last year. 92% of all contracts were fixed-price.

The growing use of Other Transactions (OTs) underscores the limitations of traditional FAR-based procurement when engaging with non-traditional vendors. Despite years of calls to expand access to flexible contracting pathways, OT adoption has accelerated in recent years and gained meaningful traction — SVDG is not surprised that the increase in OTs coincides with a rise in total awards to NatSec100 companies. This trend presents a clear opportunity for acquisition leaders and lawmakers to institutionalize and scale the contracting mechanisms that are demonstrably accelerating innovation delivery.

-

Recent executive actions and pending legislation (e.g., FORGeD Act, SPEED Act) signal intent to transform acquisition processes and accelerate innovation adoption through significant structural changes.

SVDG is optimistic—but cautious. Past reform efforts often fell short. The key question now: Will DoD leadership continue empowering program managers and acquisition officials to sustain FY23–25’s growth in innovation investment?

Ensuring follow-through will be essential to building a defense acquisition system that’s fit for purpose in an era of strategic competition.

-

NatSec100 companies are not evenly distributed across the OUSD(R&E) list of 14 critical technology areas. The NatSec100 continues to be dominated by companies in AI, software, cyber, and space. Other priority tech areas, such as microelectronics, quantum, hypersonics, and directed energy—remain underrepresented.

This concentration presents both a challenge and an opportunity. SVDG routinely hears from private capital that stronger demand signaling is required in order to deploy new capital. While the Department of Defense has traditionally relied on startups for innovative software and primes for complex hardware, this bifurcation may no longer serve emerging mission needs. As national security challenges demand advanced capabilities in areas like quantum science and engineered biology, investment will increasingly be the key to unlocking their potential.

America and the World are at a critical crossroads: comprehensive Action and Leadership are imperative now... Protecting our country goes way beyond just the military and includes, among other items, grid security, data centers, communications and cybersecurity in general... We need to allow greater flexibility on the reallocation of money; i.e., to continuously innovate (buy the newest drones and other items).

Jamie Dimon

CEO, JPMorganChase

Chairman and CEO Letter to Shareholders, 2024 Annual Report

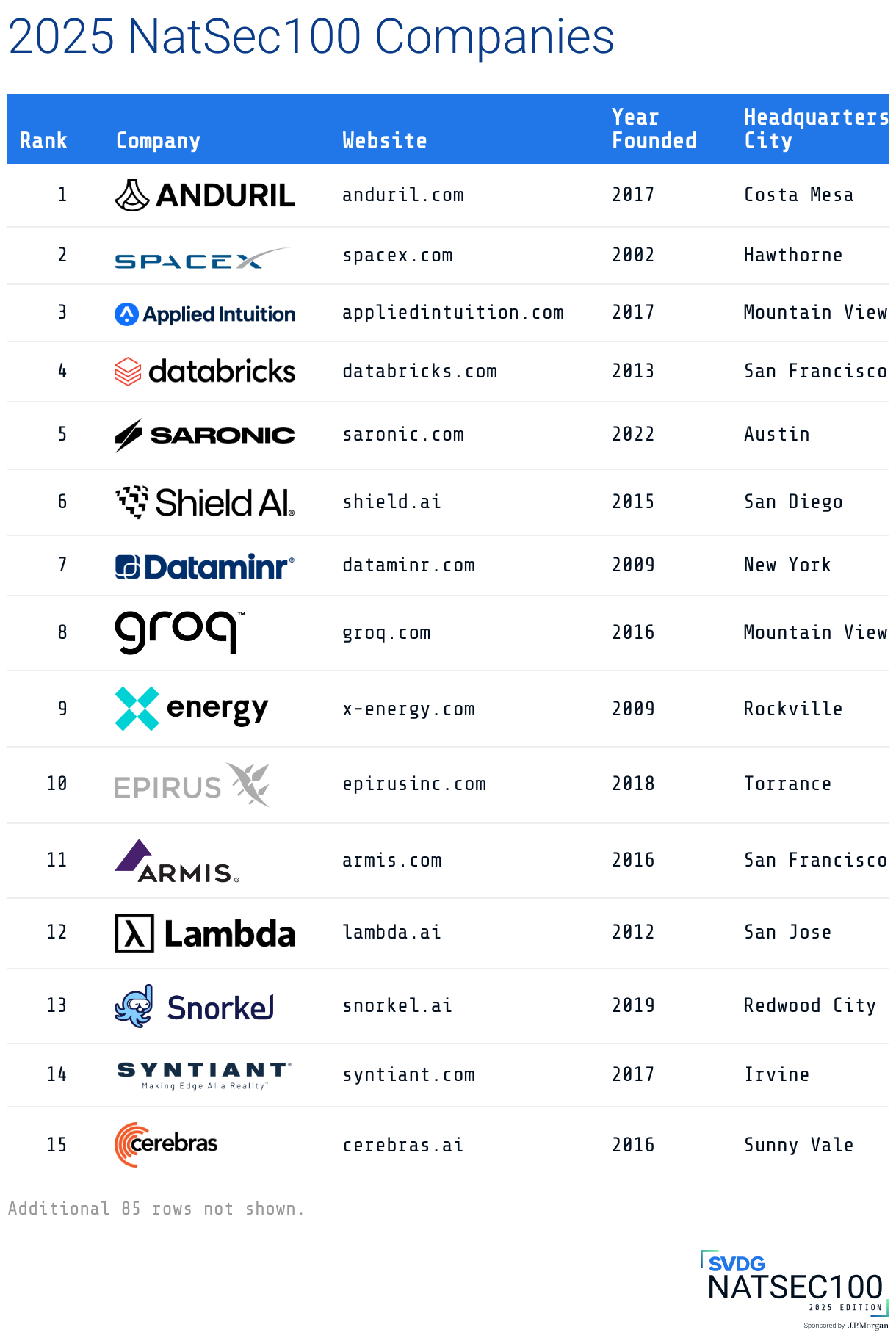

2025 NatSec100 Companies

Stats to Date

$28.6B

Total Federal Awards

Prime, Sub, OTA, SBIR/STTR

18% from 2024

$25.8B

Federal Prime

$1.8B

$798M

Federal Subcontract

$199M

Federal SBIR Awards

Federal OTA

$70.1B

Total Private Capital Raised

32% from 2024

$8.3 years

Average Age of Company

$41.5B

Gap between Total Private Capital and Total Federal Awards

Datawrapper Table Test